Request for Free Demo

What is EWayBill

Date: 2020-10-13

The E Way Bill (EWB) is an electronic bill which can be generated on an e-way bill portal. In February 2018 GST E-way billing method was introduced by Ministry of Road Transport and Highway for a trial period of 14 days. Within this trial period of E-way bills, 11581 transporters generated more than 28 lakhs GST E-way bills. From 15th April 2018, the e-way bills started rolling out in 4 different phases. The implementation of GST E-way bills has not only given transparency but also increased the efficiency and decreased the transportation time.

As per section 68 of the GST act, e-way bills shall be generated when the consignment or amount of goods which has to be moved from one place to another exceeds the threshold limit of 50,000 INR.

E-way bill shall be generated against the following things

In the above cases, so mentioned supply is the movement of goods for any consideration paid or if there is an exchange of goods or/and transfer from branch to another.

There are different conditions when a person or company has to generate an e-way bill and they are:

In a case when there is a movement of consignment by a registered person e-way bill can either be generated by the recipient or the registered person as the case may be.

When the registered person transfers the goods or consignment to a transporter for the movement then e-way bill shall be generated by the transporter.

In the case when there is a movement of goods or consignment by an unregistered person then the e-way bill shall be generated by him only.

When there is a supply of good from an unregistered person to registered person then it will be assessed as the registered person is moving the goods and hence registered person is liable to generate the e-way bill.

Any taxpayer who wants to generate an e-way bill for the consignment must have an access first on the Government portal.

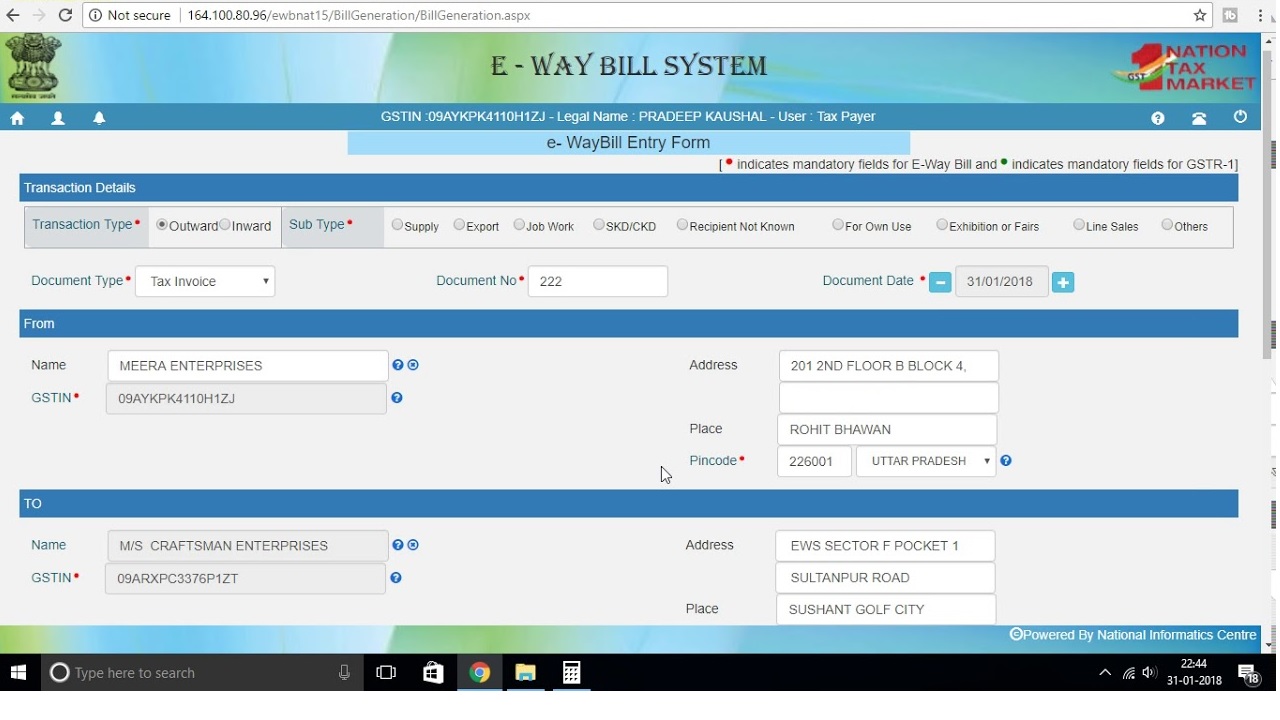

Below is the format of an e-way bill

The validity of an e-way bill is determined from the date of its generation.

E-way bill validity depends on two major things

| Conveyance Type | Kilometers (Distance) | E-Way Bill Validity |

|---|---|---|

| Normal cargo | Up to 100 kilometres | one day |

| Every additional 100 Kilometer | one additional day | |

| Over dimensional cargo | Up to 20 kilometres | one day |

| Every additional 20 kilometers | one additional day |

The validity of an e-way bill can be extended either before 4 hours of its expiry time or after 4 hours after expiry. So, in total there are 8 hours with the holder of an e-way bill to extend the time period of expiry. If in case the holder or taxpayer do not extend its validity he will be penalized accordingly.

If the transporter is moving without an e-way bill he must be penalized. There is two type of penalties which are imposed on the transporters they are as discussed.

In this case when there is a movement of consignment without an invoice and e-way bill the transporter shall be penalized either with 10,000 INR or amount of tax evaded, whichever is higher.

When the taxpayer is failed to comply with the policies so mentioned the vehicle and goods can be detained and seized without any notice. However, both can be released if the owner wishes to pay the full tax or half the price of goods.

There are some exempted goods which do not require an e-way bill. They are as mentioned

Q1. Whether a person can generate e-way bill without an invoice?

E-way bill can be generated by any taxpayer without an invoice if he has the following documents with them

Invoice of tax paid

Credit Notes

Delivery Challan

Bill of supply or Entry

Q2. If a taxpayer gets the notification for cancellation of EWB or for any changes done by the transporter in Part-B?

Every taxpayer who has generated the e-way bill will get the notification for the change in the Part-B as well as if there is any rejection or cancellation done. This notification will either come on their registered mobile number or the email-id or both.

Q3. How many e-way bills are required for multiple consignments that are being transported on the same vehicle?

For every different consignment that are in the vehicle for the delivery must have different e-way bills. If the transporter or in-charge fails to show the EWB than the goods of that particular consignment can be ceased.

Q4. What are different modes of generation of E-way bill?

EWB can be generated by different means they are mentioned below

By GST Suvidha Provider (GSP)

Through ASP (Application Service Provider)

Android app

By e-way bill website: https://ewaybillgst.gov.in/login.aspx

Through site-to-site integration

Q5. Is it possible to generate bulk amount of e-way bills?

Yes, any taxpayer or transporter who activated the automated platform for generating invoice can generate the e-way bill in bulk. Through this, the transporter or taxpayer whichever the case may be will be able to refrain their mistakes as well the chances of duplicate entries will also decrease.