Request for Free Demo

What is HSN Code

Date: 2020-10-13

Until 30th June, 2017, goods coding system in India prevailed in its primeval stages and thousands of products across various states had their own coding mechanisms for classifying goods, until the advent of the new generation taxation regime – GST, which to function, demands a fully uniform and organized classification of goods, applicable PAN India and which is followed internationally too. The adoption of the HSN [ Harmonised System of Nomenclature] Codes will bring utmost clarity, transparency and enhanced efficiency in the way goods were classified and understood.

Harmonised System of Nomenclature [HSN] is a six digit uniform code that classifies 5000 + products worldwide. It was thought of and developed by the World Customs Organization [WCO] with a vision of standardizing the classification of all the goods prevailing worldwide, in a logical and systematical manner. HSN plays a crucial role in the taxation of a country and helps to get the accurate rate of tax applicable on any product in a country. HSN is also referred to analyze a specific product movement across the world and assists in determining the volume of any product exported or imported.

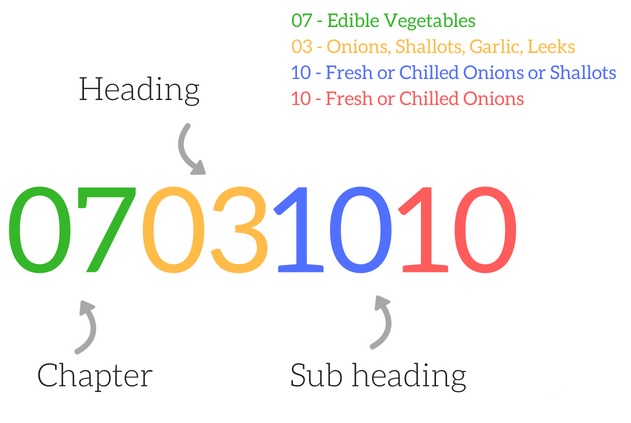

The six digit code is an organized amalgamation of different sections – drilled down to chapters – further classified into headings and sub headings.

HSN is by far the best known logical system of classification and identification of 98% + goods in the world and is widely acknowledged in 200 + countries across the world.

The new generation, GST module in India is designed for syncing only with the HSN codes and every product or service will get classified accordingly. Although, the Central Excise and Customs department has been using since 1986, however, the new GST regime has 2 more digits added to it, giving it furthermore clarity. The Indian businesses will use a 3 layered HSN configuration.

Businesses with a turnover of < 1.5 crores, do not need any HSN code.

Businesses with a turnover of > 1.5 crores but < 5 crores will use a 2 digit HSN code.

Businesses with a turnover of >5 crores will use a 4 digit HSN code.

Businesses into exports or imports will use the full 8 digit HSN code, irrespective of the turnover.

The entire HSN module consists of 21 sections, which have 99 chapters, broken down into about 1244 headings and 5224 sub-headings. The technical and technological intricacy of a product defines, which section and chapter, they should fall into. Like, all the natural products like vegetables, animal produce etc. take the first seats in the initial sections, whereas the complex products like heavy industrial machinery etc. lie towards the end. Processed cotton comes earlier than natural or uncombed cotton.

While the sections hint about the broader family, the chapters go in deep details and categorize more specifically. For instance, Section 11 talks broadly about textile and its produces while the Chapter 62 of Section 11 particularly describes accessories for men and women.

Furthermore, the chapters have been bifurcated into headings and sub-headings. All headings have a product attached to them, like, in chapter 62, heading 13 covers all types of textile handkerchiefs whereas heading 14 covers scarves and shawls of all types. Digging a bit deeper, handkerchief made of material other than textile also fall under the chapter 62 but with a different heading and the HSN code for the same is 62.13.90, where 90 is the product code for handkerchiefs made of other textile materials. The GST Council has put two more digits for a micro classification of the products. For a handkerchief made of human fiber, the HSN code is 62.13.90.10 and for a handkerchief made of silk or silk waste, the HSN code is 62.13.90.90.

The HSN Codes in GST include 233 sets of amendments bifurcated as follows:

85 in agricultural sector

45 in chemical sector

13 in wood sector

15 in textile sector

6 in base metal sector

25 in machinery sector

18 in transport sector

26 in other miscellaneous sector